Fresenius SE & Co KGaA

DUS:FRE

Decide at what price you'd be comfortable buying and we'll help you stay ready.

|

F

|

Fresenius SE & Co KGaA

DUS:FRE

|

DE |

|

C

|

CRH PLC

XBER:CRG

|

IE |

|

H

|

Heineken Holding NV

XBER:4H5

|

NL |

|

Reynolds Consumer Products Inc

F:3ZT

|

US |

|

Konami Group Corp

F:KOA0

|

JP |

|

G

|

Greif Inc

XBER:GR3

|

US |

|

H

|

Hong Kong Exchanges and Clearing Ltd

XMUN:HK2C

|

HK |

|

L

|

Loblaw Companies Ltd

F:L8G

|

CA |

|

B

|

Beiersdorf AG

SWB:BEI

|

DE |

|

L

|

Learnd SE

XETRA:LRND

|

LU |

|

Oji Holdings Corp

OTC:OJIPY

|

JP |

|

T

|

Toshiba Corp

F:TSE1

|

JP |

|

R

|

Roche Holding AG

XHAM:RHO5

|

CH |

|

H

|

HCA Healthcare Inc

SWB:2BH

|

US |

|

C

|

Chevron Corp

SWB:CHV

|

US |

|

Schibsted ASA

F:XPGB

|

NO |

|

O

|

Old Dominion Freight Line Inc

SWB:ODF

|

US |

|

F

|

Fabrinet

F:FAN

|

KY |

|

Chocoladefabriken Lindt & Spruengli AG

SIX:LISN

|

CH |

Fresenius SE & Co KGaA

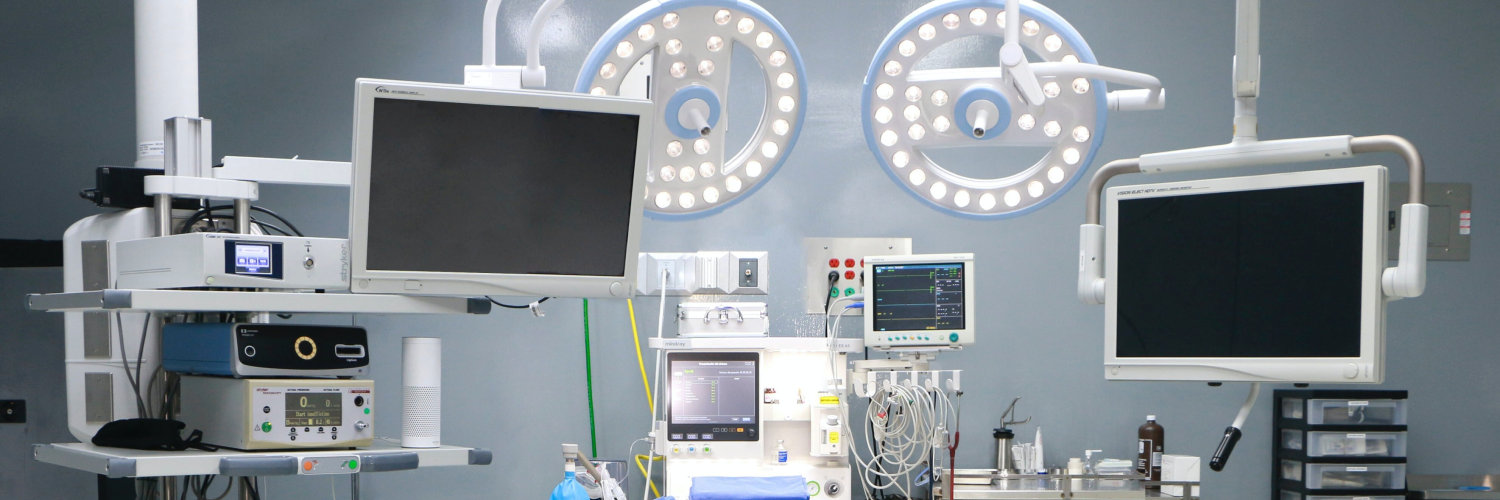

Fresenius SE & Co KGaA is a healthcare company that makes medical products and runs hospitals. Its product side, Fresenius Kabi, sells things like IV fluids, injectable medicines, clinical nutrition products, infusion pumps, and other supplies used in hospitals and clinics. Its hospital side treats patients through large hospital networks in Germany and Spain, where it provides inpatient care, surgeries, and related medical services. The company makes money in two main ways. First, it sells healthcare products to hospitals, pharmacies, and other medical providers. Second, its hospital businesses are paid by insurers, public health systems, and patients for treatment and procedures. That mix gives Fresenius a role on both sides of the healthcare system: it supplies the tools doctors need and also delivers the care itself. What makes Fresenius different is that it sits close to the core of everyday healthcare rather than selling optional consumer products. Demand for its services and supplies is tied to surgery, chronic illness treatment, and routine hospital care, which makes the business easy to understand: when hospitals need dependable medical consumables and when patients need care, Fresenius is often part of the chain.

Fresenius SE & Co KGaA is a healthcare company that makes medical products and runs hospitals. Its product side, Fresenius Kabi, sells things like IV fluids, injectable medicines, clinical nutrition products, infusion pumps, and other supplies used in hospitals and clinics. Its hospital side treats patients through large hospital networks in Germany and Spain, where it provides inpatient care, surgeries, and related medical services.

The company makes money in two main ways. First, it sells healthcare products to hospitals, pharmacies, and other medical providers. Second, its hospital businesses are paid by insurers, public health systems, and patients for treatment and procedures. That mix gives Fresenius a role on both sides of the healthcare system: it supplies the tools doctors need and also delivers the care itself.

What makes Fresenius different is that it sits close to the core of everyday healthcare rather than selling optional consumer products. Demand for its services and supplies is tied to surgery, chronic illness treatment, and routine hospital care, which makes the business easy to understand: when hospitals need dependable medical consumables and when patients need care, Fresenius is often part of the chain.

Strong start: Fresenius said Q1 2026 was fully in line with expectations and reconfirmed full-year guidance after reporting solid organic revenue growth and strong EPS growth.

Growth and leverage: Core EPS rose 13% in constant currency, helped by operating leverage, lower interest expense, and a lower tax rate, while net debt-to-EBITDA improved to 2.6x.

Kabi momentum: Kabi posted 6% organic revenue growth and a 16.7% EBIT margin, with management highlighting biopharma, nutrition, and medtech as the main growth drivers.

Helios strength: Helios delivered a 10.5% EBIT margin and 10% EBIT growth in Germany, with management pointing to higher admissions, pricing, and ongoing productivity gains.

Balance sheet: Management emphasized that the company’s stronger balance sheet gives it flexibility, but said buybacks are low on the list of capital allocation priorities.

Outlook and risks: Management stayed constructive on the rest of the year, but said the outlook still assumes a volatile geopolitical backdrop, FX headwinds, and possible second-order cost effects from the Middle East situation.